Class News

Hall of Graduate Studies tower named for David Swensen, honorary member of the Class of 1964

A $25 million gift—and a new name for the HGS tower

YAM website, March 25, 2015

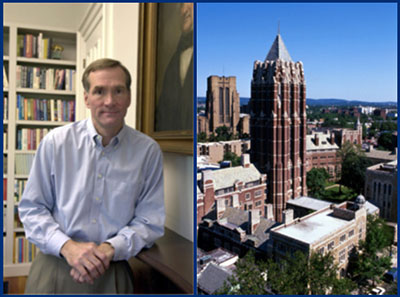

David Swensen and David Swensen Tower

Yale’s skyline is dominated by buildings named Sterling, Harkness, Kline, and Whitney — honoring people who gave money to the university in the hundreds of millions of 2015 dollars. These namesakes are being joined now by someone who has made Yale billions of dollars richer — longtime chief investment officer David Swensen ’80PhD.

The university announced today that Lisbet Rausing and Peter Baldwin ’78 have given $25 million toward the restoration of the Hall of Graduate Studies. Per their request, Yale has agreed that the 14-story HGS tower will be christened the David Swensen Tower in honor of the prodigious money manager, a Graduate School alumnus.

As we wrote in a profile of Swensen back in 2005, Yale’s endowment performance had earned it $7.8 billion more than if it had performed as well as an average university endowment during the 20 years he had been there. That number is surely bigger now that the endowment has roared back from the setbacks of the Great Recession to a new high of $23.9 billion as of last June 30.

Rausing and Baldwin’s gift will support the restoration of HGS and its transformation into a home for several small humanities departments. In 2011, Rausing and Baldwin gave $25 million to launch the Institute for the Preservation of Cultural Heritage at Yale’s West Campus. And in 2002, Rausing and Joseph Koerner ’80 gave $10 million to establish the Henry Koerner Center for Retired Faculty.

Readers interested in knowing more about David Swensen may want to read the following article from the Yale Alumni Magazine of July/August 2005.

Yale’s $8 Billion Man

David Swensen has made better returns for Yale than any portfolio manager at any university. He has a word of advice: don’t try this at home.

Last spring, Yale president Richard C. Levin ’74PhD held a cocktail reception for David F. Swensen ’80PhD, who was celebrating his 20th year as Yale’s chief investment officer. Inside the president’s official residence, posters and news clippings mounted on easels tracked the growth of Yale’s endowment from $1.3 billion to $14 billion under Swensen’s stewardship. The display culminated in a bar chart titled “Value of Key Contributors to Yale University.” The names — Harkness, Sterling, Beinecke, Mellon — were familiar, and the size of their donations, expressed in 2005 dollars — $128 million, $151 million, $263 million, $379 million — were as impressive as the campus landmarks that bear their names. Towering above them was a bar bearing Swensen’s name and an astonishing number: $7.8 billion.

Yale’s endowment has generated net investment returns that average 16.1% per year.

No one has named a Yale building after David Swensen — not yet, anyway — and it’s a safe bet that most students and alumni do not know who he is. Yet Swensen, an unassuming 51-year-old Midwesterner who did his undergraduate work at the University of Wisconsin in River Falls, has arguably made as much of a contribution to Yale as anyone in recent times. That $7.8 billion figure is the difference between the value of Yale’s endowment today, after 20 years of Swensen’s portfolio management, and what its value would be had the money grown at an average rate of return for all college and university endowments. When Yale is measured against its peers, a group of universities with multibillion-dollar endowments that includes Harvard, Princeton, Stanford, and MIT, the difference is smaller but still impressive: Swensen and his team turn out to have generated about $4 billion in added value for the university.

Since Swensen’s arrival in 1985, Yale’s endowment has generated net investment returns that average 16.1 percent per year. “For the last 20 years, no educational institution has a better performance record than Yale,” Swensen says, matter-of-factly. By comparison, Harvard’s endowment has grown by a still very impressive 14.9 percent a year. Jack Meyer, the outgoing head of the Harvard Management Co., which manages Harvard’s money, says, “I think David is the best in the business.”

Think of it this way: a $10,000 gift to Yale made in 1985 would have grown by now to $158,328, assuming none of it had been spent. That performance handily beats stock-market returns of $95,226, as measured by the S&P 500, and bond-market returns of $44,722, as measured by a Lehman Brothers index. (It does not, however, approach the record of Berkshire Hathaway, the company run by the legendary investor Warren Buffett, in which a $10,000 investment would have grown to $413,721.) What makes Swensen’s record more noteworthy is that Yale’s returns have been generated by a portfolio with less risk than the one he inherited and less volatility than an investment in stocks. That is an investor’s dream — less risk and higher return.

Swensen’s thinking has reshaped the way other large-scale institutional endowments are managed; Harvard, Princeton, and Stanford would be poorer institutions had their portfolio managers not followed his lead, and people he helped train at Yale now manage money at the Rockefeller Foundation, the Carnegie Corporation, and Bowdoin College. In 2000, Swensen wrote the definitive book on institutional investing, called Pioneering Portfolio Management: An Unconventional Approach to Institutional Investment.

In August, the Free Press will publish his second book, a guide for individual investors called Unconventional Success: A Fundamental Approach to Personal Investment. Books offering investment advice are plentiful, but this one is likely to make waves, for a couple of reasons. The first is that Swensen’s track record as an investor lends him authority, and the second is that he is so clearly troubled about what he sees as the immorality — there’s no other word for it — of the American investment business as it’s practiced today. His most pointed criticism is directed at the mutual-fund industry which, as he shows, has been no friend to investors. “Overwhelmingly,” Swensen writes, “mutual funds extract enormous sums from investors in exchange for providing a shocking disservice.” That is, mutual funds charge their investors big fees and usually fail to deliver returns that beat the market.

While mutual-fund managers are his favorite target, Swensen is also bothered by other businesspeople who do not share his unyielding moral sense. General Electric’s former CEO, Jack Welch, with his retirement perks; Merrill Lynch analysts who tout the stocks of their own investment-banking clients; and Charles Schwab fund marketers who encourage investors to chase hot performance — all come under fire in the book. So does the Bush administration’s proposal to create personal Social Security accounts, which Swensen views as irresponsible.

Perhaps because Swensen prides himself on his integrity, he bristles when critics come after him. Student activists have accused Yale of investing in oil and timber operations that are environmentally irresponsible. Others, including a U.S. senator, blamed Yale for backing a hedge fund that planned to pump, export, and sell water in the San Luis Valley of Colorado. Yale’s unions, in particular, have targeted the university, saying it is needlessly secretive about its investments. “They’re doing a fabulous job of making money, but what are the social and environmental costs?” asks Ben Begleiter '04PhD, who works for the group that is trying to organize a graduate students' union. Two years ago during a union strike, eight retired employees seeking higher pension benefits occupied Swensen’s office overnight. They refused to believe him when he tried to explain that he had no sway over their pensions.

Wall Street money managers suffer no such indignities. They also earn much more than Swensen does. In 2002-2003, the last year for which public records are available, he was paid about $1 million, making him Yale’s highest-paid employee. But his counterparts at Harvard, which has outsourced its portfolio management to a private company, earn $15 million to $20 million a year. And hedge-fund managers in the private sector earn even more — typically, 20 percent of their investment returns, which can net the best of them $100 million or more in a good year. So it’s no wonder that, when Swensen spoke to alumni in Manhattan last year, a businessman named David “Tiger” Williams asked him a tongue-in-cheek question. “If you were running a hedge fund with your asset base, and you had generated the kinds of returns you have, you'd be worth around $800 million,” Williams said. “What’s wrong with you?”

What is wrong with David Swensen? “A genetic defect,” he says, smiling. He is only half-joking. The oldest of six children, Swensen comes from a family of academics. His father and grandfather were chemistry professors. His father was also dean of the college of arts and sciences at the University of Wisconsin-River Falls. His mother became a Lutheran minister after raising their children. His parents organized international cultural exchanges and helped resettle more than 100 foreign refugees in rural Wisconsin. “I learned from my parents that there are a lot of important things in life you don’t measure in dollars and cents,” Swensen says. Growing up in the state that produced progressive politicians like Robert LaFollette, Bill Proxmire, and Gaylord Nelson, Swensen recalls, “I wanted nothing more than to be a U.S. senator from Wisconsin.”

Instead, Swensen came to Yale in 1975 as a graduate student in economics and fell in love with the place. “I’d never met so many smart people who loved ideas, who loved to engage in intellectual debate,” he says. As a freshman counselor, he began a lifelong friendship with a Berkeley College freshman named Dean Takahashi. For the past 19 years, Takahashi '80, '83MPPM, has worked as Swensen’s deputy in the investments office. Altogether, about 20 people work in the office, and they hire and oversee roughly 100 outside managers who invest Yale’s money.

As a grad student, Swensen studied with two gifted economists who would help shape his life. James Tobin, a Nobel Prize winner with a modest mien and a deep moral sensibility, became his mentor and good friend until Tobin’s death in 2002. William Brainard, the Arthur Okun Professor of Economics, advised him, first on his dissertation and later on work in the investments office. Swensen’s dissertation, “A Model for the Valuation of Corporate Bonds,” led him to Wall Street, where he spent six years in corporate finance at Lehman Brothers and Salomon Brothers. “I liked the competitive aspects of Wall Street,” he says, “but — and I’m not making a value judgment here — it wasn’t the right place for me because the end result is that people are trying to make lots of money for themselves. That just doesn’t suit me.”

When Yale needed a new endowment manager in 1985, Brainard, then the university provost, recommended Swensen. He was an unorthodox hire. Only 31, he had never managed an institutional portfolio. But he was smart, and analytical, and willing to challenge conventional wisdom. Recalls Brainard: “It might have looked like an odd choice, but I didn’t have any anxieties about it.”

The endowment had been poorly managed for some time. From 1968 to 1979, a period of high inflation and poor stock market performance, its purchasing power declined by 45 percent. Spending had been frozen, and an outside company formed by Yale to manage the endowment had been fired.

Here, a word about how the endowment works. The $14 billion investment pool is actually an amalgam of thousands of funds donated for a wide variety of purposes. These funds support the 28 Sterling Professors, underwrite scholarships, and finance so many graduation prizes that they cannot all be given out in one day. They also pay for upkeep of the bells in Harkness Tower and the plantings of annuals on campus, the costs of theatrical productions in Yale College and the salaries of the head coaches of football, track, and swimming. About one-fifth of the money is unrestricted, and all of it eases the pressure on the rest of the university budget.

Schools with the biggest endowments get richer because both their relative and absolute returns tend to be better. So the gap that separates Harvard, Yale, and Princeton from the rest of the Ivies is wider than ever, and likely to grow wider still.

Every endowment manager has two goals. “If you are going to be a good steward of endowment assets,” Swensen explains, “you need to care both about preserving the purchasing power of the portfolio and about providing as much for the operating budget as you possibly can.” Yale uses a complex formula to calculate how much it can spend from the endowment each year; the rate, which is set by the Yale Corporation, has increased from 4.5 percent in 1982 to 5.25 percent today, reflecting confidence that the endowment will continue to grow at a healthy pace.

The heart of the endowment manager’s job is to allocate assets to different classes of investments. In the early 1980s, Yale held more than three-quarters of its money in U.S. stocks, bonds, and cash. This was a mistake, Swensen and Takahashi decided; the analytical tools Swensen had learned as a graduate student indicated that the portfolio was not sufficiently diversified. (Tobin used to explain portfolio theory by saying it boiled down to “Don’t put your eggs in one basket.”) By putting too much money into U.S. stocks and bonds, Yale was both taking on too much risk and missing out on opportunities in such investment classes as foreign stocks; real assets, which include real estate, oil and gas, and timber; private equity, which includes venture capital and buyout firms; and a category known as “absolute return,” hedge funds that try to capitalize on market inefficiencies and special situations such as distressed businesses. As Swensen explains it, those other asset classes deliver “equity-like” returns, but because they are not correlated with U.S. equities, they cushion the portfolio against losses when the stock market goes through its inevitable down cycles.

How diversified have Yale’s holdings become? Over the years, the endowment has invested in public companies like the cable giant Comcast and the insurance firm UnitedHealthcare, startups like Cisco, Yahoo, and Amazon before they went public, newly privatized firms in Russia and small companies in China, high-end office buildings such as the John Hancock Center in Chicago, timberland in Maine and Idaho, even a resort in Tucson. (The women’s golf team got to practice there for free one year.) Most recently, according to the Wall Street Journal, Yale took a big stake in the Kimpton Hotel and Restaurant Group, a fast-growing chain of hip boutique hotels, many of which operate under the Hotel Monaco brand. By diversifying beyond U.S. stocks, which are widely followed, Swensen has been able to seek opportunities in less liquid, less efficient markets where the sophisticated investment managers that he hires could gain a competitive advantage.

In retrospect, Swensen’s approach sounds sensible, but at the time it was revolutionary. “No institutions were managing money in accordance with what finance theory would tell us,” he says. “It just wasn’t done.” Len Baker '64, a Silicon Valley venture capitalist and member of the Yale Corporation, says that one of Swensen’s strengths is his willingness to think for himself. “He doesn’t get his information from consensus,” Baker says. “He does his own thing.” Having his trusted friend Takahashi at his side helps a lot; they enjoy challenging each other’s ideas, as well as upending conventional wisdom. “They do a lot of introspection,” says Josh Lerner, a Harvard Business School professor who wrote about Yale’s methods for an HBS case study. “And they have the self-confidence to chart a distinctive path.”

Asset allocation is driven mostly by quantitative analysis. But the second major job of an endowment manager is picking the right asset managers — a matter of judgment, more art than science. Swensen has a demonstrable gift for both. Remarkably, Yale’s outside managers outperform the benchmarks in each of the asset classes. It’s famously difficult, for example, for active managers of U.S. equities to beat the stock market indexes because the markets are generally efficient; employing active managers who run up transaction costs and charge management fees is usually a losing proposition for investors. Knowing that, Yale used to invest heavily in index funds. Now it invests with managers like Glenn Greenberg '68, whose firm, Chieftain Capital, has managed endowment money since 1992.

Before hiring an outside manager, Swensen does lots of due diligence. “People I went to junior high school with had been contacted by Yale,” jokes Doug Shorenstein, chair and chief executive of the Shorenstein Company, a real-estate firm that invests for Yale. Swensen accompanies investment managers when they visit companies, and he will call CEOs to see which investors they think best understand their business. “You want people of high integrity, high energy, high intellect, people who are obsessed with the market,” he says. “You like to see independence, a modestly strong contrarian bent.” He also wants Yale’s outside managers to have their own money in the funds they manage for their clients, and he prefers those who specialize. One manager focuses on small energy companies in Canada. Another specializes in biotechnology. Most run concentrated portfolios. Greenberg, for instance, has his own money and his clients' in just six public companies.

Over the past ten years, Yale’s domestic equity managers as a group have outperformed the Wilshire 5000, a broad gauge of publicly traded stocks, by 5.5 percent a year. Yale’s managers have also outperformed their benchmarks in the categories of absolute return, fixed-income bonds, real assets, and the biggest winner of all, private equity, which earned Yale a whopping 37.6 percent annual return over the past ten years. This included Yale’s single most profitable investment to date, a stake in a telecommunications company called Cerent. Yale bought its stake for $400,000 and collected $130 million when the company was sold to Cisco in 1999. By investing with Silicon Valley venture firms like Kleiner Perkins Caufield & Byers and Sutter Hill Ventures (whose partners include Len Baker), Yale rode the late 1990s technology boom for all it was worth.

Because it was diversified, the endowment also held up well after the bubble burst and the public markets collapsed. In 2002, a year when most endowments suffered heavy losses, Yale’s portfolio gained a respectable 0.7 percent.

“The endowment growth,” says Rick Levin, “is by far the most important single financial contributor to what we have been able to accomplish over the last decade.” When Swensen became chief investment officer in 1985, Yale could safely spend just $46 million of endowment money a year, representing about 10 percent of its operating budget. Last year, the university spent $502 million from the endowment, about 31 percent of its budget. The difference amounts to well over $1 million a day, and its impact is tangible: renovated campus buildings, a $1 billion investment in facilities for science, engineering, and medicine, dramatic increases in financial aid for low-income and international students, and new global initiatives. Charles Ellis '59, a member of the Yale Corporation and chair of its investment committee, says, “Can you imagine Rick Levin doing anything like the great job he’s done if he didn’t have the discretionary resources to do it?”

Or, as a rival portfolio manager said when the Chronicle of Higher Education asked him about Swensen: “He’s too damn good for the rest of us.”

Last spring, as students in a class in Yale’s School of Management debated the ethics of making money from sweatshops, their lanky, boyish-looking lecturer listened impassively. One student argued that no one should profit from exploiting child labor. Another called that “anti-capitalist,” saying child labor has been part of the industrialization of every country, including the United States.

David Swensen teaches this class on institutional portfolio management every year, along with a Yale College class on investing. He’s not obligated to teach, but does so because he enjoys it. His comment on the sweatshop issue: “Sometimes the behavior of management is within a legal framework, but it’s not a business practice that you want to be associated with.”

There is no way for anyone but Swensen and his team to know whether Yale profits from sweatshops (even if we could agree on how to define the term), because the endowment customarily does not identify its holdings or disclose the names of its investment managers. Only a limited amount of data is released as part of Yale’s IRS filings. Transparency has become a watchword in corporate America, but not at Yale, much to the dismay of some campus activists.

Ethical investing has been debated at Yale for more than 30 years. Swensen’s mentors, Tobin and Brainard, led a seminar on the issue in 1969. Three years later, law professor John Simon '53LLB and two graduate students wrote The Ethical Investor: Universities and Corporate Responsibility, the first book on the topic. In 1972, Yale also became “the first major university to resolve this issue by abandoning the role of passive institutional investor,” according to the New York Times. It formed an Advisory Committee on Investor Responsibility (ACIR) made up of students, faculty, and alumni. Between 1978 and 1994, at the committee’s urging, Yale divested shares of 17 companies doing business in South Africa.

School of Management professor K. Geert Rouwenhorst says ACIR has not recommended any changes in investment policy since he became chair two years ago. Final authority on investment policy rests with the Yale Corporation. With few upgrades to the ethics policy lately, Yale has in effect reverted to a passive role — at least as far as an outsider can tell. The fact is, it’s difficult to know what role, if any, the endowment plays as an owner of stocks and companies because it discloses so little. Begleiter, the union activist, says: “Because there is a complete lack of disclosure about where the endowment is invested, that forestalls a debate or conversation about how Yale makes its money.” Swensen says that Yale trusts its money only to investors with the highest ethical standards, but there’s no way to verify his claim. Indeed, Yale will not even say how it votes on shareholder resolutions on the proxy ballots of companies in which it owns stock. The Securities and Exchange Commission recently required mutual funds to disclose their proxy votes, but its decision does not apply to universities or foundations.

Other universities are more open, and some have gone further than Yale when it comes to ethical investing. Harvard divested tobacco stocks; Yale has not, though Swensen says there were no tobacco holdings as of his last yearly review. This spring Harvard divested from PetroChina, a company tied to the Sudanese government. Williams College created a “Social Choice Fund” for donors who want social and environmental issues taken into account. Swarthmore College publishes its holdings online.

Robert A. G. Monks, a prominent shareholder advocate, says universities are obliged to become more responsible owners. He argues that active institutional owners could help to steer business in ethical directions on issues ranging from CEO pay to global warming. “By their silence, the great universities have allowed shareholder advocacy to be marginalized,” Monks says. “If Harvard and Yale were to say, 'We’re owners and we’ve got to take responsibility,' then everyone would follow that norm.”

Swensen responds that Yale has committed to managing its timber holdings sustainably, and the investment managers he hires do speak up about the corporations in which they hold stakes. (Glenn Greenberg publicly objected when Comcast tried to merge with Disney.) Swensen also says that he welcomes the campus debate, now unfolding under the auspices of ACIR, over the university’s holdings in companies doing business in Sudan. (U.S. companies cannot do business there, so the holdings are probably few, says Swensen; he is identifying them.) ACIR routinely makes the call on social responsibility proxy votes.

Swensen argues that disclosing Yale’s holdings would erode the university’s competitive edge. “To the extent that there’s value in the information that an active manager gathers, you dissipate that value in making the information public,” Swensen says. Disclosure might also bring unwanted attention to asset managers. “If people discover that one of our managers is investing for Yale, that becomes a Good Housekeeping Seal of Approval, and the manager comes under pressure to take more money.” Nor, he says, would it be practical for him to take on the task of setting social and environmental policy for all of Yale’s investment managers, let alone for the companies they invest in. “I don’t want to be in a position where I’m trying to figure out the right social consequences and the right environmental consequences and then try to engineer the portfolio to achieve those,” he says. “That’s not my job.”

Swensen chose to write his new book for individual investors because, he says, “It’s very, very difficult for investors to get good advice. Most providers have an ax to grind.” Brokers want people to trade stocks, insurance agents want to push their products, and the mutual fund industry and its vast network of distributors — well, don’t get Swensen going on that.

Swensen’s critique of the for-profit mutual fund industry is devastating. He argues persuasively that most mutual funds and their managers benefit from high fees, sales commissions, portfolio turnover, and, above all, amassing more assets. Those actions all run counter to the interests of individual investors. Moreover, most funds fail even to achieve their basic goal of beating market returns. They are charging a lot of money for lousy results. “Overwhelming evidence,” writes Swensen, “proves the failure of the for-profit mutual-fund industry.”

Consider just one problem he identifies — the so-called 12b-1 fees, which mutual funds charge to their investors to pay for marketing and distribution costs. The fees pay for, among other things, those full-page ads touting the latest hot funds that appear in newspapers and magazines. Their purpose, of course, is to bring in new investors, who make the fund company more profitable. But as funds grow bigger, managers inevitably find it difficult to buy bigger stakes in their existing investments without driving up the cost. “There’s an inverse relationship between size and performance. Period,” Swensen says. The SEC has permitted 12b-1 fees even though they are clearly not in the interests of investors. Swensen writes: “Shame on the SEC for allowing 12b-1 fees, shame on the [fund] directors for approving them, and shame on the mutual funds for assessing them.” Brokers who charge sales commissions for the mutual funds they offer only stack the deck further against their unsophisticated clients. “Sensible investors avoid the brokerage community,” he writes.

None of this will win Swensen friends on Wall Street. Several Yale Corporation members and members of its investment committee have close ties to the fund and brokerage businesses. So be it, Swensen says. “I don’t want to make people feel badly about what they do, but I just think that the entire mutual fund industry has failed,” he says. “The clients lost, and the people who run the mutual funds made a lot of money. That’s scandalous. It’s a failure of the system. I know at times that I sound intemperate, but I feel so passionately about this.”

Swensen’s book could also thrust him into the debate over privatizing Social Security accounts. In Unconventional Success, he shows that most individual investors fail to follow the most basic investment precepts. Most trade too much, buy high, sell low, chase past performance, and fritter away money on excessive fees and sales charges. Given that, it’s tough to argue that giving individuals more control over their retirement accounts is sound policy. “You’re asking people to take responsibility for an activity in which they’ve demonstrated failure,” Swensen says.

As for Swensen’s own future, his hope is to keep doing what he’s doing. A divorced father of three, he has carved out a good life for himself in New Haven, coaching his kids' soccer and Little League teams. Swensen says he is happy with his job, with his colleagues, with the chance to teach, and with the satisfaction of helping the university to prosper. “I’m going to be here for as long they’ll have me,” he says. Past performance, as they say, is no guarantee of future results, but chances are that Yale will be happy to have him for a long time.